February 24, 2026

Public company executives at the director level and above often accumulate significant employer equity through RSUs, equity grants, and ESPPs. Over time, choosing to retain those shares can lead to meaningful concentration in a single company’s stock.

As income and net worth increase, charitable intent often expands alongside it. At the same time, concentrated equity positions may become more pronounced. Charitable Planning with Employer Stock allows executives to evaluate philanthropic goals and concentrated equity exposure within the same strategic framework, rather than addressing each issue in isolation.

Aligning Philanthropy with Equity Compensation

Charitable giving isn’t solely a philanthropic decision. When a significant portion of wealth is tied to employer equity, charitable decisions may intersect with portfolio concentration, tax exposure, and long-term financial goals.

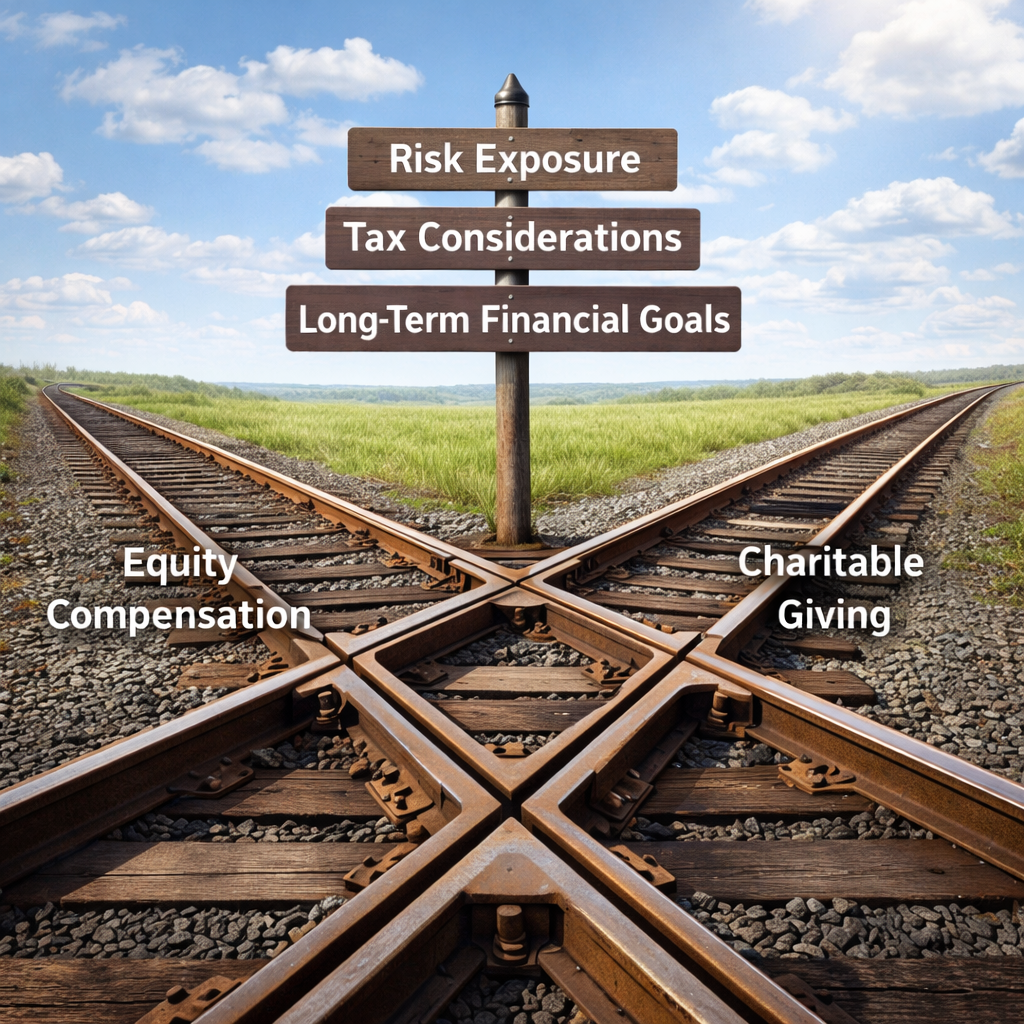

For senior executives, evaluating charitable planning within the broader context of equity compensation can bring greater clarity. Rather than being viewed as a standalone activity, giving can be viewed through several integrated lenses:

Risk Exposure

- What level of concentration exists in employer stock?

- How might donating shares affect overall portfolio exposure?

- Can philanthropic goals align with efforts to manage concentrated positions?

Tax Considerations

- How much embedded gain have my appreciated shares accumulated?

- How does donating stock differ from donating cash?

- How may timing of gifts interact with income fluctuations or major liquidity events?

Long-Term Financial Goals

- How does gifting stock compare with retaining shares for future liquidity needs?

- How might charitable decisions affect retirement timing considerations?

- Does income variability influence the timing of larger gifts?

Why Executives Consider Gifting Employer Shares

Over years of compensation growth, executives often accumulate appreciated employer stock. As those positions grow, charitable giving may become part of a broader discussion around portfolio concentration, tax exposure, and long-term financial priorities.

For some executives, donating shares instead of cash may intersect with broader efforts to manage concentrated stock risk while supporting meaningful causes. The potential impact depends on factors such as embedded gains, income variability, and overall liquidity needs.

Charitable decisions in this context are not often isolated. They often form part of a larger tax-efficient giving framework that considers retirement timing, estate objectives, and compensation structure.